CONTENTS

The AI Revolution in Finance Reaches a Critical Juncture

Real-time Payments Require Real-time Action

Open Banking and Embedded Finance Open Opportunities Galore

Time to Redraw Customer Journeys for ‘Lifestyle Banking’

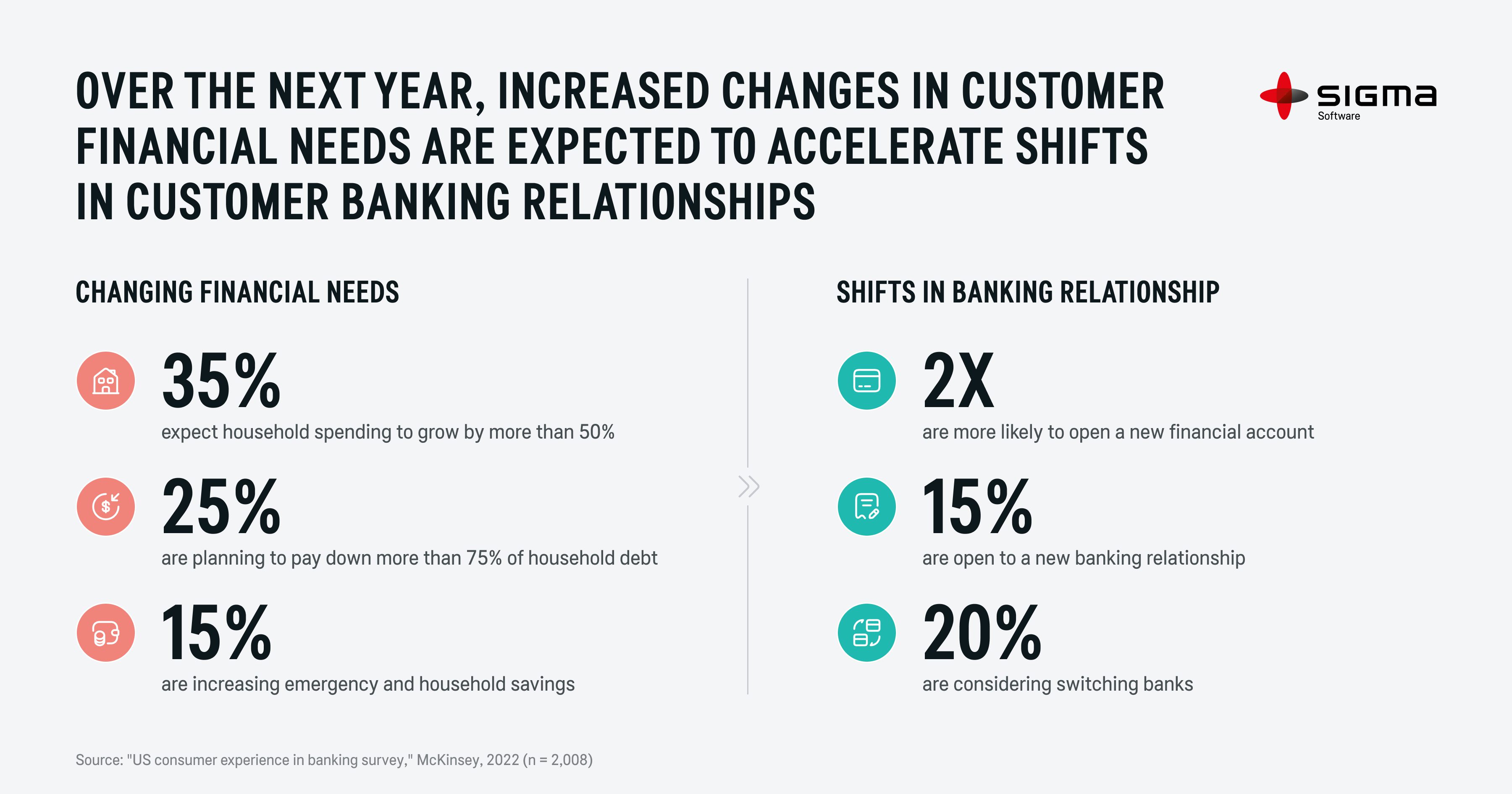

Customer-driven Product Development Sets the Path to Profitability

Digital Excellence Requires Process Excellence

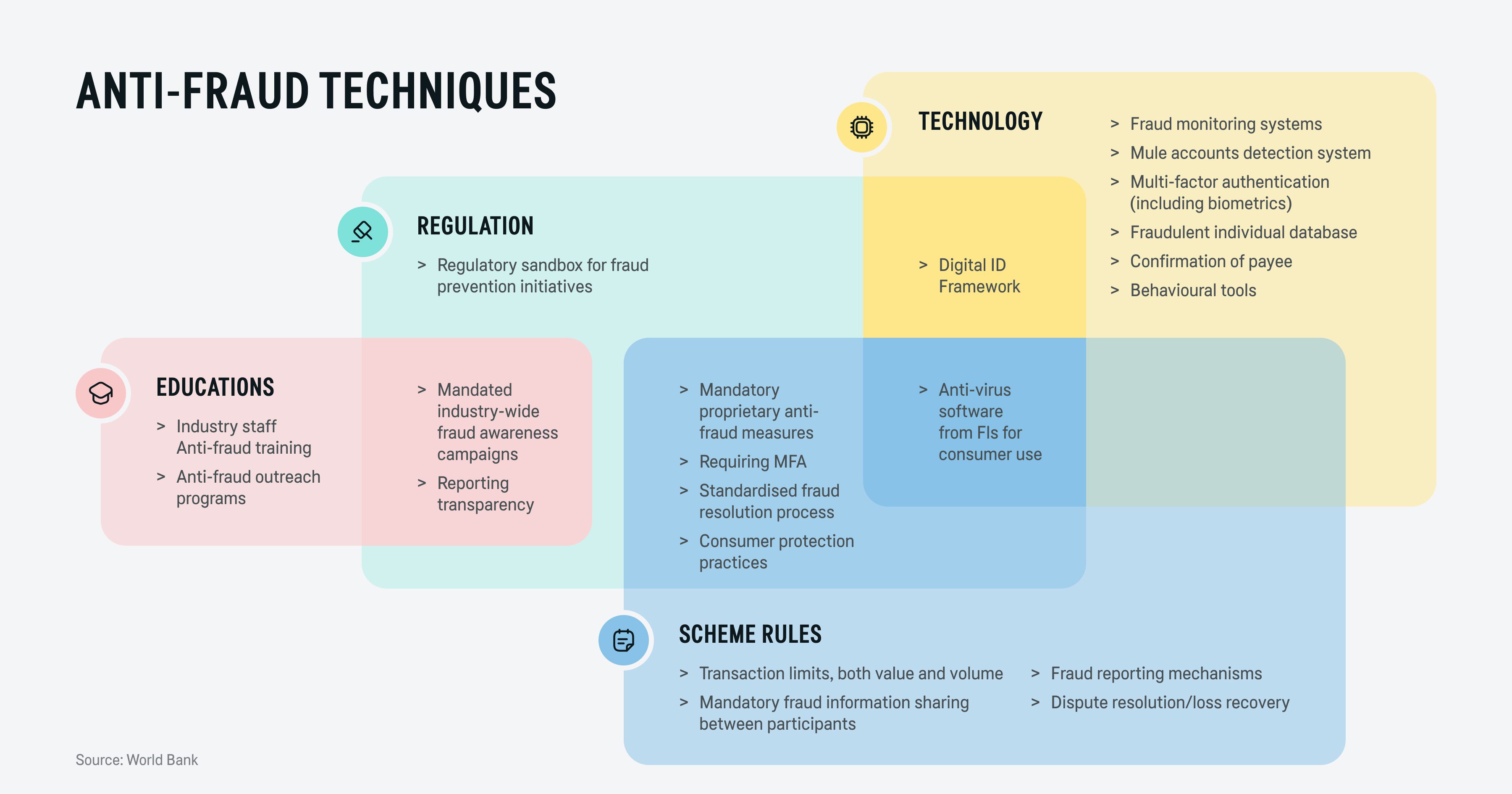

Align Your Infrastructure with New Regulations

One Last Crypto-penny for Your Thought: the Bond with Blockchain